North Macedonia is often marketed as “simple and tax-friendly.” That can be true—but it is not a substitute for structured legal diligence. If you are pursuing buying a company in North Macedonia or acquiring any type of assets, you need a lawyer who is experienced in mergers & acquisitions to guide you through the process and to produce an objective legal due diligence in North Macedonia. This will ensure that the target shares or target assets are straightforward: confirm that what you are paying for is legally real, transferable, and enforceable.

North Macedonia remains a frontier market that is still integrating into global business flows. Combined with its simple and competitive tax regime, expanding business opportunities, and an evolving corporate governance framework, the country has attracted a steady and significant influx of foreign direct investment. According to the National Bank of the Republic of North Macedonia, total inward FDI stock reached EUR 8.4 billion as of 31 December 2024.

However, the country continues to face structural challenges. These include an inefficient justice system, a persistent gray economy, informal business practices, assets kept off the books, weak record-keeping, and inconsistent management standards. These realities make a thorough and properly structured legal due diligence process essential when acquiring assets, purchasing companies, investing in development projects, or entering into partnerships in North Macedonia.

This is precisely why foreign investors need an experienced local lawyer who understands not only the legal framework in North Macedonia, but also how business is actually conducted on the ground. A proper due diligence process requires knowledge of regulatory risks, enforcement realities, documentation gaps, and structural weaknesses that may not be immediately visible. At the same time, it requires cultural awareness.

Many transactions of this scale are still relatively new in the Macedonian market. Some founders and counterparties operate based on long-standing relationships, informal understandings, or simplified agreements. A strategic local counsel must therefore guide the process carefully—explaining why structured due diligence and contractual safeguards are necessary, while ensuring that the other side does not feel attacked, distrusted, or buried under unnecessary bureaucracy. Successful transactions in North Macedonia often depend as much on nuance and communication as on legal matters.

What legal due diligence is and why it must be integrated

Legal due diligence is the process of confirming that the target’s legal foundations match the commercial story. It differs from: i) Financial and tax diligence (numbers, debt-like items, tax exposures, quality of earnings); and ii) Technical diligence (asset condition, engineering compliance, grid connection, design vs as-built). To ensure a comprehensive review, we as corporate lawyers in Skopje work closely with trusted external tax and financial experts, as well as specialized technical partners—particularly in the construction and energy sectors—so that clients receive an integrated, full-scope due diligence assessment.

A deal team should integrate these workstreams, especially in emerging or fast-evolving markets. A technical finding (for example, a deviation from a permitted design) can become a legal closing blocker if it voids an operational permit or triggers a re-approval process. Integration is how you turn findings into transaction design.

The strategic posture matters. The best due diligence lawyer acts as a deal architect: mapping risk, designing solutions, and converting diligence findings into enforceable closing mechanics (conditions precedent, escrows, targeted indemnities), rather than producing a report that sits on a data room shelf.

Industries where legal due diligence is most common in North Macedonia

Investors most often run deep diligence where assets are land-heavy, permit-heavy, or compliance-heavy.

Real estate development and land acquisition

In real estate and development transactions, due diligence in North Macedonia rests on two pillars: registration and buildability.

The starting point is always the property’s legal status. The Agency for Real Estate Cadastre operates the official e-services portal through which investors obtain title sheets, cadastre extracts, and historical ownership data. A proper review verifies ownership, co-ownership ratios, registered mortgages, pledges, easements, rights of way, long-term lease agreements, annotations of disputes, and enforcement notices. In development projects, the situation is often more complex because land is frequently acquired from multiple owners. That multiplies diligence layers: each seller’s title history, each encumbrance, each third-party right must be mapped and, where necessary, terminated, renegotiated, or structurally managed. If banks hold mortgages or negative pledges, negotiations with secured creditors become part of the transaction architecture.

The second pillar is urban planning and permitting status. Urban planning in North Macedonia is a dynamic, continuous process linked to the adoption and implementation of detailed urban plans. In acquisitions, a simple statement that “a building permit exists” is not sufficient. Due diligence must validate the entire permitting chain: zoning compliance, urban planning documentation, location conditions, construction permits, utility approvals, and confirmation that construction matches approved designs. It is increasingly important to review not only the existence of permits but also the procedural integrity of how zoning rules were adopted and how construction permits were issued. In recent years, projects have faced annulments of zoning plans or revocation of permits due to procedural irregularities, which can materially affect valuation and bankability.

Where value depends on anticipated rezoning or density upgrades, diligence extends beyond current planning documents. Investors must assess the feasibility of future urban plan amendments, taking into account environmental regulation, nature protection laws, cultural heritage constraints, and infrastructure capacity. This often requires parallel consultation of urban planning statutes, ecological legislation, and sector-specific restrictions. For developers, real estate due diligence is therefore not merely a title check; it is a structured risk assessment of ownership integrity, encumbrance management, regulatory durability, and long-term buildability under both existing and projected planning frameworks.

Distressed projects

Distressed projects are a due diligence hotspot because risk escalates quickly once liquidity problems begin. While many distressed transactions in North Macedonia involve unfinished real estate developments, similar issues arise in energy projects, manufacturing facilities, hospitality assets, infrastructure ventures, and even financial portfolios. Delays, unpaid contractors, secured creditors, and regulatory exposure can rapidly complicate the investment landscape.

If insolvency risk is part of the investment thesis, the bankruptcy framework and available restructuring tools must be reviewed early. It is essential to determine whether formal insolvency proceedings have been opened, how secured creditors rank, and whether a transaction can be structured as a clean asset acquisition or requires navigating existing liabilities within the company.

In parallel, creditor positions must be mapped carefully. This includes reviewing registered pledges and mortgages, enforcement proceedings, intercreditor arrangements, and any contractual restrictions on transfer. A key question is whether the project can be legally completed under its existing structure or whether value can only be preserved through an asset sale or restructuring. In distressed situations, transaction structuring becomes as important as the legal review itself.

Energy sector and infrastructure

Over the past several years, a significant portion of legal due diligence engagements in North Macedonia has been concentrated in the energy sector, particularly in solar photovoltaic (PV) projects. Most transactions involve the acquisition of special purpose vehicles (SPVs) holding project rights, permits, land interests, and grid connection approvals, although certain transactions are structured as asset deals. The typical target is a ready-to-build (RTB) project in Macedonia, where key milestones such as urban planning compliance, construction permits, energy approvals, and grid connection terms have already been secured. There have also been acquisitions of operational or near-completion projects.

Energy transactions in North Macedonia are regulator-driven and require close review of the applicable licensing and regulatory framework. The Energy Regulatory Commission of the Republic of North Macedonia acts as the sector regulator under the Energy Law, while the Ministry of Energy, Mining and Mineral Resources publishes the relevant legislative framework, including the Energy Law and its implementing regulations.

A thorough due diligence review in solar transactions typically focuses on license validity and transferability, grid connection agreements, feed-in or market-based arrangements, construction compliance (design vs. as-built), land rights, environmental approvals, and change-of-control implications under the regulator’s Rulebook on Licenses. In practice, careful analysis of these elements determines whether the project is bankable, transferable, and capable of reaching commercial operation without regulatory disruption.

Financial companies, microfinance, and leasing

In recent years, the microfinance sector in North Macedonia has grown significantly, with a number of financial companies operating in the field of consumer and SME lending. Many of these institutions participate on secondary markets for receivables, including B2B and, in certain models, C2C platforms where loan portfolios or individual claims are sold, assigned, or serviced through structured arrangements. As a result, due diligence in microfinance transactions is supervision-driven and portfolio-focused.

A typical legal due diligence in this sector begins with verification of licensing and regulatory compliance under the Law on Financial Companies and, where applicable, the Law on Leasing. This includes confirmation that the company holds valid authorization, complies with capital and reporting requirements, and appears in the relevant public registers maintained by the competent authorities. Beyond licensing, a core component of the review is the loan portfolio itself: sampling receivables, assessing enforceability of loan agreements, reviewing interest calculation methodologies, checking security instruments (pledges, guarantees, promissory notes), and verifying proper registration of collateral where applicable.

Particular attention is paid to the legal mechanics of assignment and transfer of claims. This includes reviewing framework agreements for portfolio sales, notification procedures to debtors, servicing arrangements, data protection compliance, and any restrictions on transferability. Consumer protection compliance is critical. The review typically examines adherence to financial consumer protection rules, transparency of fees and interest, advertising practices, default procedures, and alignment with mandatory disclosure requirements. Any history of regulatory inspections, administrative sanctions, or court disputes is also analyzed.

In addition, due diligence in this sector often covers AML/CFT compliance systems, internal governance and credit approval policies, IT systems used for portfolio management, outsourcing arrangements, and data processing practices. In transactions involving distressed or non-performing portfolios, enforceability trends, litigation exposure, and recovery rates become central valuation drivers. Because microfinance businesses are highly regulated and reputation-sensitive, the legal review must assess not only formal compliance but also operational risk, portfolio integrity, and regulatory exposure that could affect continuity or valuation post-acquisition.

IT and intellectual property transactions

In IT-sector transactions, intellectual property due diligence often determines whether the acquirer truly owns the product it believes it is buying. Unlike asset-heavy industries, value in technology companies frequently lies in software code, proprietary algorithms, databases, trademarks, domain names, and know-how embedded in the development team. A structured IP review, therefore, begins with confirmation of registered rights. The State Office of Industrial Property provides access to trademark and industrial property records and publishes the Law on Industrial Property. Due diligence should verify ownership of trademarks, pending applications, opposition proceedings, licensing arrangements, and any encumbrances over IP rights. Domain registrations and brand usage consistency should also be reviewed to avoid post-closing disputes.

For software-driven businesses, copyright protection is central. While software is protected under copyright law rather than patent law in most cases, ownership is not automatic in transactional terms. The key diligence question is whether the company holds valid and properly assigned rights from developers, contractors, or outsourced teams. This includes reviewing employment agreements, IP assignment clauses, contractor agreements, open-source usage policies, and code repository access. The World Intellectual Property Organization (WIPO Lex) provides a consolidated reference to North Macedonia’s copyright legislation, but the practical focus is contractual chain-of-title verification. If developers were engaged as freelancers without proper assignment clauses, ownership may remain fragmented or challengeable.

In addition to formal IP rights, IT due diligence must examine data protection compliance, software licensing terms, SaaS subscription structures, customer contracts, and restrictions on transferability upon change of control. Open-source components should be screened for copyleft risks that could affect commercialization. Where the company’s value depends on proprietary platforms, due diligence should confirm the exclusivity of code ownership, the absence of third-party infringement claims, and the protection of trade secrets. In IT acquisitions, IP diligence is not a checklist exercise; it is a structural verification that the company’s core digital assets are legally controlled, transferable, and defensible after closing.

Heavy industry and production

In heavy industry and production transactions, environmental diligence must begin at an early stage. Industrial assets carry operational, regulatory, and legacy exposure that can materially affect valuation and post-closing risk. The Ministry of Environment and Physical Planning administers the integrated environmental permit regime and provides guidance on the A and B permit system, which distinguishes installations based on capacity, environmental impact, and compliance obligations. A-type permits typically apply to larger installations with a significant environmental footprint, while B-type permits cover smaller but still regulated facilities. Confirming whether the installation holds a valid and transferable integrated permit, and whether operations align with the approved operational plan, is a core diligence priority.

Beyond permit existence, the review must assess compliance history. This includes inspection reports, administrative measures, pending proceedings, emission thresholds, waste management practices, water usage approvals, hazardous substance handling, and environmental impact assessment (EIA) documentation where applicable. The Ministry’s regulatory framework covers environmental protection, air quality, waste management, water law, and related secondary legislation. Any deviation from permit conditions or reporting obligations can trigger fines, operational suspension, or revocation risk. For brownfield sites, historical contamination exposure and remediation obligations must also be evaluated, as liability may attach to the operator or asset holder depending on transaction structure.

Industrial due diligence also extends to workplace safety, labor compliance, and technical conformity of machinery. Production facilities often involve complex equipment subject to safety certifications, inspection regimes, and maintenance logs. Investors must verify whether key assets are owned outright, leased, subject to retention-of-title clauses, or pledged to lenders. In cross-border acquisitions, regulatory alignment with EU environmental standards is particularly relevant, especially where exports depend on compliance certifications. In heavy industry transactions, environmental and regulatory exposure can outweigh pure commercial considerations; therefore, diligence must integrate legal, technical, and operational review to ensure that the asset is not only profitable but lawfully sustainable.

Tourism and hospitality investments

Tourism and hospitality investments in North Macedonia require heightened regulatory scrutiny, particularly in protected or historically sensitive areas. Assets located in or around protected zones may be subject to layered restrictions that directly affect development rights, renovation scope, or operational flexibility. UNESCO recognizes the Natural and Cultural Heritage of the Ohrid region as a site of outstanding universal value, reflecting the unique convergence of natural ecosystems and cultural heritage. Projects in and around Lake Ohrid, therefore, operate within a sensitive regulatory environment. In parallel, the Cultural Heritage Protection Office publishes the Law on Protection of Cultural Heritage, which establishes approval requirements, conservation standards, and restrictions applicable to protected sites and surrounding buffer zones.

Due diligence in tourism projects must go beyond basic title verification. Investors should assess zoning parameters, urban planning constraints, coastal and environmental limitations, protected-area designations, and whether the property falls within a cultural monument or archaeological zone. Renovations, expansions, façade alterations, and even interior modifications may trigger special approvals from heritage or environmental authorities. In addition, hospitality assets require review of operational permits, categorization status (e.g., hotel star ratings), sanitary approvals, food safety compliance, and concession arrangements where applicable. Failure to comply with these sector-specific rules can result in fines, suspension of operations, or refusal of expansion permits.

Where investment value depends on redevelopment or repositioning, it is essential to evaluate not only current compliance but also the feasibility of planned upgrades under heritage and environmental frameworks. Projects near Lake Ohrid in particular must be assessed against environmental protection laws, water management regulations, and UNESCO-related preservation standards. For a more detailed overview of legal requirements when buying, starting, or operating a café, hotel, restaurant, or other hospitality business in North Macedonia, you may consult our dedicated article on hospitality and tourism investments, which provides a step-by-step regulatory guide for investors and operators.

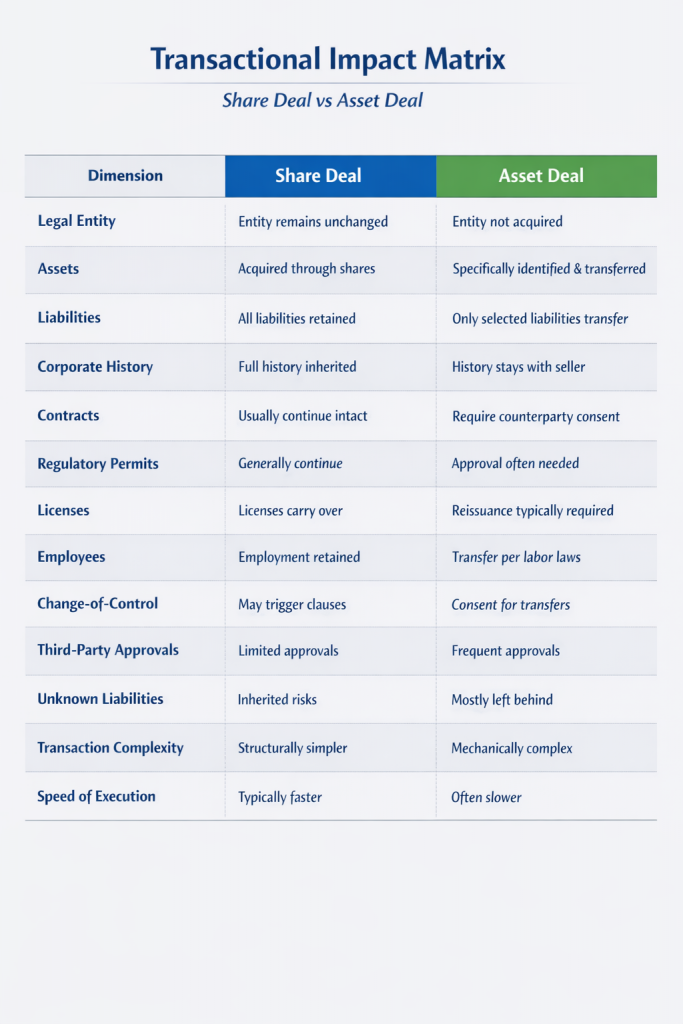

Share deal vs asset deal: how the structure changes the review

Deal structure is a foundational element of any acquisition, as it determines the scope of due diligence, the allocation of risk, and the mechanics of post-closing implementation. In practice, acquisitions in North Macedonia are most commonly structured either as a share deal or as an asset deal, although hybrid and restructuring-based transactions also occur in specific circumstances.

A share deal (share purchase transaction) involves the acquisition of ownership interests in a company. The legal entity remains intact; only the shareholders change. As a consequence, all assets, rights, obligations, and liabilities of the company—known and unknown—remain within the entity after closing. The acquirer steps into the position of the seller as shareholder and indirectly assumes the company’s historical exposure. Due diligence in a share deal is therefore entity-wide. It encompasses corporate governance, historical compliance, tax records, employment relationships, litigation, contractual arrangements, regulatory permits, encumbrances, and contingent liabilities. The principal advantage of a share deal lies in its structural simplicity: contracts, permits, and licenses generally remain with the entity, avoiding the need for individual transfers. It may also preserve regulatory continuity and tax positions. The principal disadvantage is the inheritance of historic risk. Any undiscovered liability remains within the company unless contractually allocated through warranties, indemnities, or price adjustments.

An asset deal (asset purchase transaction), by contrast, involves the acquisition of specific assets and selected liabilities of a business without acquiring the legal entity itself. The buyer identifies and purchases defined assets—such as real estate, equipment, intellectual property, receivables, or contractual rights—while leaving behind unwanted liabilities within the seller’s entity. The principal advantage of an asset deal is risk isolation: historic corporate liabilities typically remain with the seller. However, this structural clarity comes at the cost of greater transactional complexity. Each asset must be individually transferred. Real estate requires cadastre registration; intellectual property assignments may require recordals; contractual rights often require counterparty consent; pledges must be released or restructured; and regulatory permits may require approval or reissuance. In regulated sectors such as energy, construction, or environmental operations, permits may not be automatically transferable, and formal authority approval may be required. Thus, while the legal exposure may be narrower, the execution and documentation burden may be significantly higher.

In addition to share and asset deals, transactions may be structured as mergers, demergers, or spin-offs under corporate law, and in distressed cases through enforcement or bankruptcy sales. Joint ventures and minority investments are also common, where control is shared rather than fully transferred. Each structure affects due diligence scope, regulatory approvals, creditor involvement, and tax treatment. In practice, however, mergers and demergers are less frequently used in North Macedonia for transactional purposes. Although legally possible, they are typically slower and more procedurally burdensome, requiring formal restructuring plans, creditor notifications, statutory waiting periods, and multiple registrations. As a result, investors generally prefer share or asset deals, which offer greater speed and transactional flexibility.

The choice between these structures is not merely technical; it is strategic. Share deals prioritize continuity and administrative efficiency but require deep historical review and robust contractual risk allocation. Asset deals prioritize liability segregation but demand careful mapping of transfer mechanics and regulatory approvals. Hybrid or restructuring-based models may be appropriate where the target holds multiple business lines or where insolvency risk must be managed procedurally. In the Macedonian context, the optimal structure depends on the nature of the target, the regulatory framework, the investor’s risk tolerance, and the long-term operational plan.

Typical legal risks in the Macedonian market

Typical legal risks in the Macedonian market often mirror what investors see elsewhere, but they appear in distinctly local forms—driven by documentation gaps, informal practices, and inconsistent compliance culture.

A recurring theme is record-keeping risk: internal corporate records, contracts, and management practices may not match what is reflected in official filings. This is why diligence must start with a reconciliation exercise—aligning the company’s internal documentation with registry outputs from the Central Register of the Republic of North Macedonia (company status, filings, and beneficial ownership). Due diligence should never assume that “the registry is correct” or that “the company’s folder is complete”—it must test both against each other.

A second risk category is hidden claims and security interests. Foreign buyers are often surprised by pledges over receivables, inventory, equipment, or other rights that can exist even where the business appears profitable. The Central Register maintains pledge registration services and issues certificates based on pledge registry data, which should be part of any baseline screening. Missing a pledge can create immediate deal fragility: a lender or pledgee can have enforcement leverage that effectively turns a healthy company into a distressed situation overnight. Related risks include undisclosed shareholder arrangements, side letters, off-registry transfers, or “silent partners” who later surface—especially in founder-led SMEs. Add to that the practical reality that some businesses may have “off-the-books” elements (assets, revenues, employment arrangements), or may have “cut corners” to obtain permits, approvals, or licensing—creating a later revocation/annulment risk if irregularities are discovered by authorities.

Third, investors must treat disputes, enforcement, and insolvency signals as core diligence items, not an afterthought. Litigation exposure and enforcement actions can materially affect bankability, operations, and cash flow.

Because these risks cannot always be eliminated by diligence alone, a well-structured Macedonian transaction typically combines (i) verification tools and (ii) deal protections. Deal protections include conditions precedent (e.g., pledge releases, permit confirmations, third-party consents), escrow/holdbacks, indemnities, robust representations and warranties (including ownership, encumbrances, compliance, permits, and related-party dealings), and where the risk profile justifies it, specific security packages (pledges, guarantees, step-in rights) to protect the investor if third parties later assert rights or if a regulatory issue materializes.

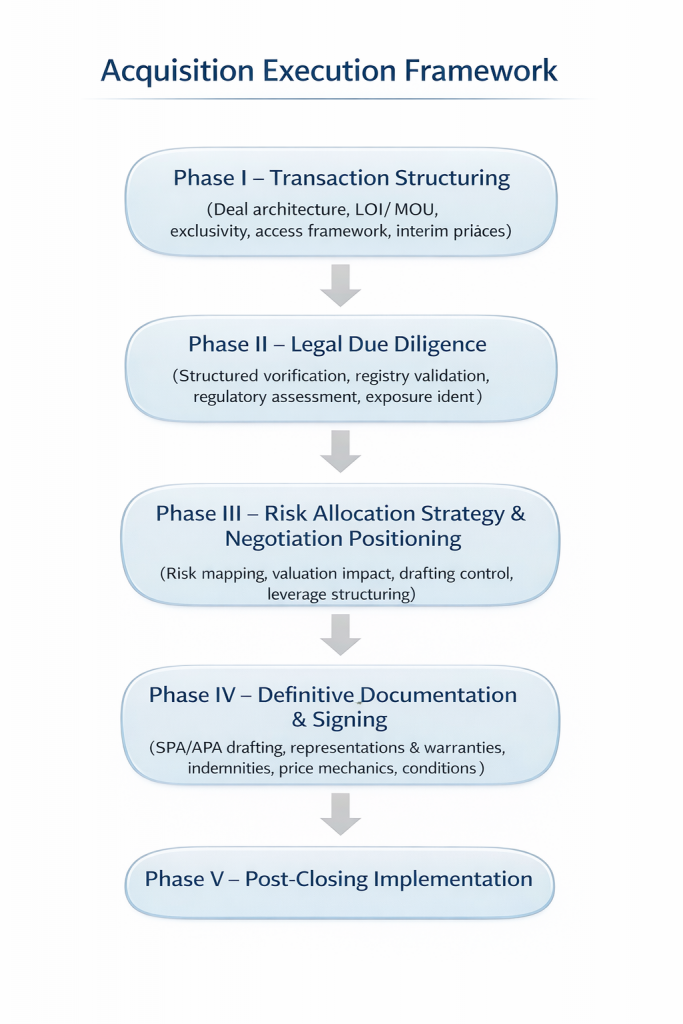

Our Transaction Workflow – Structured, Phased, and Risk-Controlled

A well-designed workflow keeps the transaction moving while maintaining control over legal and regulatory risk. In our practice, we structure acquisitions in clearly defined phases. Each phase has a purpose, a timeline, and a risk-management objective.

Phase 1 – Structuring and MOU / LOI

We begin with a detailed Memorandum of Understanding (MOU) or Letter of Intent (LOI). This document is not symbolic. It defines:

- The proposed structure (share deal, asset deal, hybrid).

- Scope of due diligence.

- Timelines and milestones.

- Access to documents and data room obligations.

- Confidentiality framework.

- Exclusivity period.

- Indicative price logic and adjustment principles.

Where the transaction involves upfront payments, deposits, staged consideration, or sensitive assets, we may recommend interim protection mechanisms. Depending on the case, these can include pledge arrangements, escrow structures, share freezes, negative pledge undertakings, or contractual restrictions preventing disposal of key assets during negotiations. In certain structures, preliminary security ensures that the seller cannot dilute, encumber, or dispose of the target while diligence is ongoing.

The objective of this first phase is clarity. Structure and protection come before investigation.

Phase 2 – Due Diligence Execution

Once structure and access are agreed, the transaction moves into verification. In this phase, we test the seller’s commercial narrative against documents, registry records, and regulatory reality.

A. Types of Due Diligence We Conduct

We structure diligence depending on risk appetite and deal context. Typical formats include:

- High-Level Red Flag Review: Focused on identifying material deal breakers: ownership, encumbrances, regulatory status, litigation exposure.

- Standard Transactional Due Diligence: Comprehensive review across corporate, contractual, employment, tax, regulatory, IP, and dispute areas.

- Deep-Dive / Risk-Control Review: Expanded historical analysis, forensic review of documentation gaps, regulatory procedures, permit issuance processes, and compliance culture.

The chosen scope depends on deal size, investor appetite, sector, and timeline.

B. Sources of Information

Our diligence relies on three coordinated information streams:

- Company-provided documentation: We review internal corporate records, shareholder agreements, key commercial contracts, employment files, regulatory permits, financing arrangements, and intellectual property documentation to understand how the business presents itself structurally and operationally.

- Independent verification: We cross-check this information against external sources, including corporate registry data, beneficial ownership filings, pledge registrations, cadastre extracts for real estate, regulatory authority confirmations, and court or enforcement records to validate accuracy and identify discrepancies.

- Representations and sworn confirmations (where proportionate): In smaller or lower-risk transactions, and where objective exposure appears limited, certain matters may be supported by formal seller representations or sworn statements. However, in higher-value or regulated acquisitions, registry-backed and authority-based verification remains essential.

By reconciling internal documentation with independent sources, this structured approach reduces reliance on informal assurances and converts commercial representations into verifiable facts.

Phase 3 – Risk Mapping and Negotiation Positioning

Once due diligence findings are consolidated, the transaction enters its strategic phase. At this stage, information becomes leverage. We categorize risks, distinguish between structural issues and manageable exposures, and determine which findings affect valuation, which require contractual protection, and which can be operationally mitigated post-closing. The objective is not merely to report risks, but to transform them into negotiation tools.

To maintain a strategic advantage, we strongly prefer to draft the first version of the transaction agreements. Controlling the initial draft allows us to frame the legal architecture of the deal, define the allocation of risk, and set the narrative within which negotiations unfold. When the other side reacts to our structure rather than imposing its own, the discussion naturally takes place within a framework that already reflects the investor’s priorities. This approach is particularly important in markets where documentation culture may vary and where informal practices can influence expectations.

During this phase, due diligence findings are translated into concrete contractual mechanisms. Price adjustments, escrow arrangements, indemnities, extended warranty periods, and carefully designed conditions precedent are aligned with identified risks. Known weaknesses are either priced, secured, or ring-fenced. Regulatory uncertainties are tied to conditional approvals. Pledge releases, permit confirmations, and third-party consents are integrated into the closing roadmap. In short, Phase 3 converts factual analysis into structured advantage, ensuring that the transaction agreement does not merely record a deal, but actively protects the investment.

Phase 4 – Negotiation and Deal Architecture

Phase 4 is where structure and risk analysis are converted into binding commitments. The focus shifts entirely to negotiating and finalizing the transaction documentation in a way that protects the investor while preserving commercial momentum. At this stage, pricing mechanics, payment sequencing, security arrangements, and risk allocation clauses are carefully aligned with the findings of the due diligence.

Purchase price can be structured in multiple ways depending on the risk profile and bargaining power of the parties. In straightforward transactions, the price may be paid in full at closing. In higher-risk or performance-driven transactions, staged payments, deferred consideration, or earn-out mechanisms may be appropriate. In cross-border or enforcement-sensitive scenarios, escrow structures or holdbacks are frequently used to secure potential claims. Where debt-like items or working capital exposure exist, completion accounts or locked-box mechanisms may be implemented to ensure pricing integrity.

Representations and warranties are tailored to reflect the Macedonian risk landscape. Title, encumbrances, permit validity, tax compliance, employment exposure, litigation, and regulatory adherence must be precisely addressed. Where specific issues have been identified during diligence—such as pending audits, permit irregularities, or potential third-party claims—targeted indemnities are negotiated. Conditions precedent are structured to require release of pledges, confirmation of regulatory approvals, and completion of critical registrations before funds are fully released.

In share deals, the negotiation emphasis typically lies in managing inherited liabilities through warranty coverage and indemnity frameworks. In asset deals, attention shifts toward defining the exact perimeter of transferred assets, ensuring proper consent mechanics, and allocating risk for any asset that fails to transfer as expected. The agreement must not only document the transaction, but actively safeguard the investor against the structural and cultural risks identified earlier in the process.

Phase 5 – Registrations and Implementation

The final phase is execution and formal registration. At this stage, negotiated conditions precedent are satisfied, security interests are released or restructured, regulatory approvals are obtained, and ownership is formally transferred. Proper sequencing is critical. Closing mechanics must align with registry procedures and, where applicable, regulatory timelines.

In a share deal, implementation is typically straightforward. The transfer of shares is registered with the Central Register, beneficial ownership data is updated, and any required FDI notifications are completed. Because the legal entity remains unchanged, most contracts and permits continue without reissuance. As a result, the registration stage is usually efficient and limited in scope.

In an asset deal, implementation is often more complex and may extend over months. Each asset requires its own transfer mechanics. Real estate must be registered with the Cadastre. Intellectual property may require recordals. Contracts may require assignment consents. Regulatory permits—such as construction, environmental, or energy approvals—may require authority confirmation or formal transfer approval. Where multiple institutions are involved, coordination becomes a key part of execution.

For this reason, while share deals tend to be simpler at the registration stage but heavier in historical due diligence, asset deals may appear cleaner from a liability perspective yet involve significantly more operational and administrative complexity after signing. A properly structured transaction anticipates these implementation realities from the outset.

Risk appetite, cultural nuance, and post-acquisition risk mitigation

Diligence depth should match investor profile:

A speed-oriented investor focuses on deal-breakers and closes fast. A balanced investor completes all core checks but uses materiality thresholds. A risk-control investor treats compliance system quality as a closing condition.

This alignment is the core of investment risk assessment Macedonia: decide which legal uncertainties you will own, and price them explicitly.

Culturally, some sellers still see diligence as mistrust. The best practice is to communicate the “why” early: diligence is how you close quickly, finance efficiently, and avoid re-trading later.

After closing, risk mitigation becomes operational:

- Clean up corporate housekeeping and delegated authorities.

- Build compliance calendars for permits and reporting.

- Align governance and policies (including IP hygiene and contractor controls in tech deals).

- Monitor disputes and creditor actions.

Plan Your Investment with Legal Clarity

orth Macedonia offers real opportunity, but opportunity without structure creates exposure. Whether you are buying a company in North Macedonia, acquiring assets, investing in a development project, or entering a joint venture, legal due diligence is not a formality—it is the mechanism that confirms that what you are paying for is legally real, transferable, and enforceable. In a frontier yet fast-evolving market, disciplined structuring, rigorous verification, and strategic negotiation are what separate successful transactions from expensive lessons.

If you are considering an acquisition or investment in North Macedonia, we would be pleased to guide you through the process with clarity, precision, and commercial focus.

📞 Call us: +389 70 257 879

📧 Email: contact@boshnjakovski.com

🌐 Website: www.boshnjakovski.com

Free Consultation

Law is complicated matter. It can cause you a big problem. Let us help you!

[…] For a comprehensive breakdown of our due diligence procedures, including our methodology, scope of review, and practical risk-mitigation strategies, please consult our detailed Due Diligence Guide. […]